This is one of the most common (and most misunderstood) situations in today’s market. The reality is, there are multiple ways to structure a move like this. Some are safe but limit your options. Others are more competitive but require the right strategy and guidance.

After helping hundreds of clients navigate this exact situation, we’ve found that success comes down to one thing: Choosing the right strategy before you ever start shopping.

The Short Answer

The best way to buy a home before selling yours depends on whether you can qualify to carry both mortgages, access your equity before selling, or list your current home first and shop once it is under contract. In Maryland, the strongest strategy is usually to avoid a traditional home sale contingency when possible, because sellers often value certainty over price.

Local Maryland Guidance Matters

We help move-up buyers throughout Central Maryland, including Annapolis, Severna Park, Pasadena, Arnold, Edgewater, Columbia, Glen Burnie, Stevensville, and surrounding areas. The right strategy can vary depending on how competitive the local market is, how quickly homes are selling, and how much equity you need from your current home.

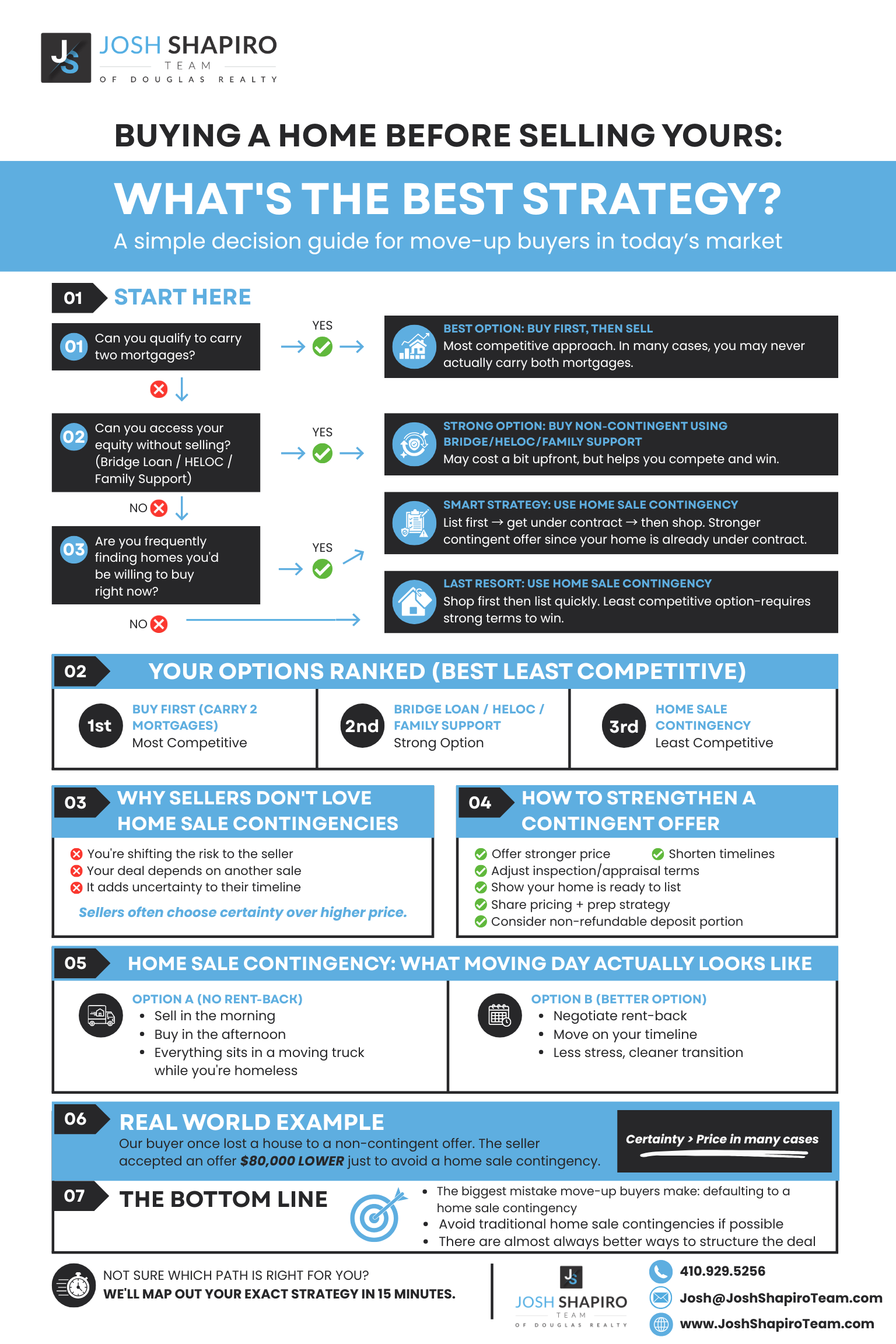

Quick Decision Guide

Use this visual as a quick overview, then read the full breakdown below to understand which strategy makes the most sense for your situation.

Can You Buy Before You Sell?

In many cases—yes.

The first step is speaking with a trusted local lender to review your income, savings, and overall financial picture. From there, we can determine whether you’re able to carry two mortgages at the same time, even temporarily. Far more buyers qualify for this than they expect.

Many assume they need to sell first in order to access their equity for a 20% down payment. In reality, it’s often possible to:

- Purchase your next home with a smaller down payment (such as 5%)

- Move into your new home first

- Then sell your current home and apply that equity afterward

Once your current home sells, you may be able to:

- Refinance your loan

- Or recast your mortgage (a one-time principal payment that lowers your monthly payment)

What If I Need My Equity to Buy?

If you need the equity from your current home to purchase your next one, you still have several strong options—many of which allow you to avoid a home sale contingency.

Option 1: Bridge Loan

A bridge loan allows you to borrow against the equity in your current home before it sells.

- You can make a non-contingent offer

- Purchase your next home first

- Then sell your current home and pay the loan back

There are some fees and interest costs, but in many cases, this is far less expensive than losing out on homes or overpaying due to a contingency.

Option 2: HELOC (Home Equity Line of Credit)

A HELOC allows you to access a portion of your home’s equity before selling.

- Works best when set up in advance

- Can provide flexibility for down payment or reserves

Option 3: Temporary Funds from Family

This is one of the most common—and often most overlooked—solutions. Many move-up buyers are able to access short-term funds from family to bridge the gap between buying and selling. This can work in a few ways:

- A temporary loan from family to cover the down payment

- A gifted portion of funds, which allows you to qualify as a non-contingent buyer

From a lender’s perspective, gifted funds are very common and simply need to be properly documented. In practice, this allows you to make a strong, non-contingent offer, purchase your next home, and then sell your current home and repay those funds afterward. While not everyone is comfortable going this route, it is often one of the simplest and most cost-effective ways to avoid a home sale contingency.

There are often more ways to access your equity than you think—and avoiding a contingency can dramatically improve your chances of winning the home you want.

What Is a Home Sale Contingency in Maryland?

A home sale contingency means your purchase is dependent on selling your current home first. In simple terms, it’s your “get out of jail free card.” If your home doesn’t sell in time, you can exit the contract and keep your earnest money deposit. But it’s important to understand what’s really happening: You’re shifting the risk to the seller. And that’s exactly why sellers don’t love them.

How Competitive Are Home Sale Contingent Offers in Maryland?

In today’s market, contingent offers are generally less competitive. When sellers are reviewing multiple offers, the ones with home sale contingencies are often the first to be set aside—especially on well-priced homes that show well. That said, there are exceptions:

- If a home has been sitting on the market for 30+ days

- If there is little or no competition

In those cases, a contingent offer can still be successful. We’ve won plenty of contingent offers over the years—but in competitive situations, they often require stronger terms to offset the added risk.

Your Options Ranked (Best → Least Competitive)

Get Approved to Carry Two Mortgages

This is the strongest position you can be in. You can shop first, make non-contingent offers, and compete with the strongest buyers. In many cases, we can structure the timing so that you never actually carry both mortgages—it simply gives you flexibility and leverage.

Use a Bridge Loan, HELOC or Temporary Funds

If you need access to your equity before selling: A bridge loan allows you to borrow against your current home, a HELOC (home equity line of credit) can provide similar flexibility, or temporary funds from family. This allows you to make non-contingent offers while planning to sell your current home shortly after. There are costs associated with these options, but they are often far less than what buyers lose by competing with a home sale contingency.

List First, Then Buy

This is a strong middle-ground strategy. We list your home first, get it under contract, and then shop for your next home. When making offers, we can show sellers your home is already under contract, inspections are complete, and the timeline is defined. This makes your contingent offer significantly stronger.

Traditional Home Sale Contingency (Shop First)

This is the most common approach—and the least competitive. You find your next home first, submit an offer with a home sale contingency, and then quickly list and sell your current home. While this can work, it often requires offering more money, tight timelines, and concessions to the seller. In addition to being less competitive on the buying side, this approach can also reduce your leverage when selling—often leading to rushed decisions, weaker negotiations, and potentially leaving money on the table.

The Hidden Risk Most Buyers Don’t Think About

A traditional home sale contingency doesn’t just make it harder to win the home you want…

It can also cause you to leave money on the table when selling your current home. Here’s why: When you go under contract on your next home first, you’re suddenly on a clock. That pressure can lead to:

- Rushing through pre-listing prep instead of maximizing how your home shows

- Pricing more aggressively than necessary just to get a quick offer

- Feeling pressure to accept the first offer instead of negotiating

- Giving up leverage during inspection negotiations because you don’t want the deal to fall apart

At that point, you’re not negotiating from a position of strength—you’re reacting to a deadline.

Why Listing First Changes Everything

When we list your home first and secure a buyer before shopping, we take the time to prep, stage, and present your home properly. We price strategically to attract strong interest (and ideally multiple offers). We negotiate from a position of strength—not urgency. We control key terms like settlement timing and rent-back. Instead of being on your heels, we’re in control of the deal.

Bottom Line: Real estate is all about leverage. The more control we have over your sale, the better positioned you are to win on both sides of the transaction.

How to Strengthen a Contingent Offer

If a home sale contingency is necessary, there are ways to make your offer more attractive:

- Offer a stronger purchase price

- Shorten contingency timelines

- Adjust inspection or appraisal terms

- Show that your home is fully prepped and ready to list

- Provide a clear pricing and marketing strategy

- In some cases, make a portion of your deposit non-refundable

The goal is to show the seller: This is a low-risk transaction—and we’re willing to share that risk.

Timing & Logistics: What This Actually Looks Like

Coordinating two transactions takes planning. In some cases, both homes will close on the same day: You sell your home in the morning and you purchase your new home in the afternoon. While this works, it can be logistically challenging. That’s why rent-backs are often a valuable tool.

A rent-back allows you to stay in your current home after closing, move on your timeline, and avoid the stress of same-day transitions. When we list your home first, we can often negotiate extended settlement timelines (30–60 days) or additional rent-back periods. This can give you up to 2–3 months to find your next home comfortably.

Real-World Example: Why Strategy Matters

We recently had a situation where our client offered $80,000 more than another buyer—and still lost the home. The reason? Our offer included a home sale contingency. The seller chose the lower offer simply because it was more certain. This is a perfect example of how, in many cases: Sellers value certainty over price.

How to Decide What’s Right for You

- Whether you can qualify to carry two mortgages

- How much equity you need from your current home

- How competitive the market is

- How selective you are about your next home

- Your comfort level with risk

If You Don’t Want to Mess This Up

Start with a plan—not a house search. Talk to a lender first. Understand your options. Choose the right strategy. And whenever possible: Avoid relying solely on a traditional home sale contingency. There are almost always better ways to structure the process.

Why Work With Us?

We’ve helped hundreds of buyers successfully navigate this exact situation. While some strategies involve calculated risk, we know how to structure deals properly, minimize exposure, and create a high level of certainty for our clients.

Thinking about making a move?

Let’s map out your strategy before you start shopping.

Schedule a Strategy CallFrequently Asked Questions About Buying Before Selling

1. Do I have to sell my home before buying a new one?

Not always. Many buyers are able to qualify to carry two mortgages temporarily, which allows them to buy first and sell afterward. The best way to determine this is by speaking with a lender and reviewing your financial situation.

2. What is a home sale contingency?

A home sale contingency means your purchase is dependent on selling your current home first. If your home doesn’t sell in time, you can exit the contract without losing your deposit.

3. Are home sale contingencies bad?

They aren’t “bad,” but they are less attractive to sellers because they introduce uncertainty. In competitive situations, they can make it harder to win a home unless the offer is strengthened in other ways.

4. Can I make a non-contingent offer if I still own my home?

Yes. This can be done in several ways, including qualifying to carry two mortgages, using a bridge loan or HELOC, or accessing temporary funds from family to cover your down payment.

5. What happens if I buy a home but my current one doesn’t sell?

This is why planning is critical. If you’re buying without a contingency, we make sure you have a clear strategy and backup plan in place to minimize risk and ensure your home sells quickly.

6. What is a bridge loan?

A bridge loan is a short-term loan that allows you to access the equity in your current home before it sells. This lets you purchase your next home without a contingency and then pay off the loan once your home sells.

7. What is a mortgage recast?

A recast allows you to make a large lump-sum payment toward your mortgage after selling your home. The lender then recalculates your monthly payment based on the lower loan balance.

8. What is a rent-back?

A rent-back allows you to remain in your home for a period of time after closing. This is often used to make the transition between selling and buying much smoother.

9. What’s the best strategy in a competitive market?

The most competitive approach is to avoid a home sale contingency if possible. This typically means qualifying to carry two mortgages or using alternative financing options.

10. What’s the biggest mistake buyers make?

The biggest mistake is starting the home search without a clear strategy or without preparing their current home for sale. Planning ahead is critical to success.

11. Can family help me buy before I sell?

Yes—and it’s more common than most people think. Many buyers use temporary funds from family to cover a down payment so they can purchase their next home without a contingency. In some cases, these funds can be structured as a gift, which lenders usually allow as long as proper documentation is provided. This approach allows you to buy first, sell your current home afterward, and then repay those funds based on whatever arrangement you’ve made.

12. Can using a home sale contingency affect how much I get for my current home?

Yes—this is one of the most overlooked risks. When you buy first and then rush to sell your home under a contingency timeline, you may feel pressure to accept lower offers, negotiate less aggressively, or skip steps that would normally help maximize your sale price.

13. Why is listing my home first often a better strategy?

Listing first allows you to sell your home from a position of strength. You have time to properly prepare, market, and negotiate your sale—often leading to better terms and potentially a higher price. It also puts you in a stronger position when making offers on your next home, since you can show sellers your home is already under contract.